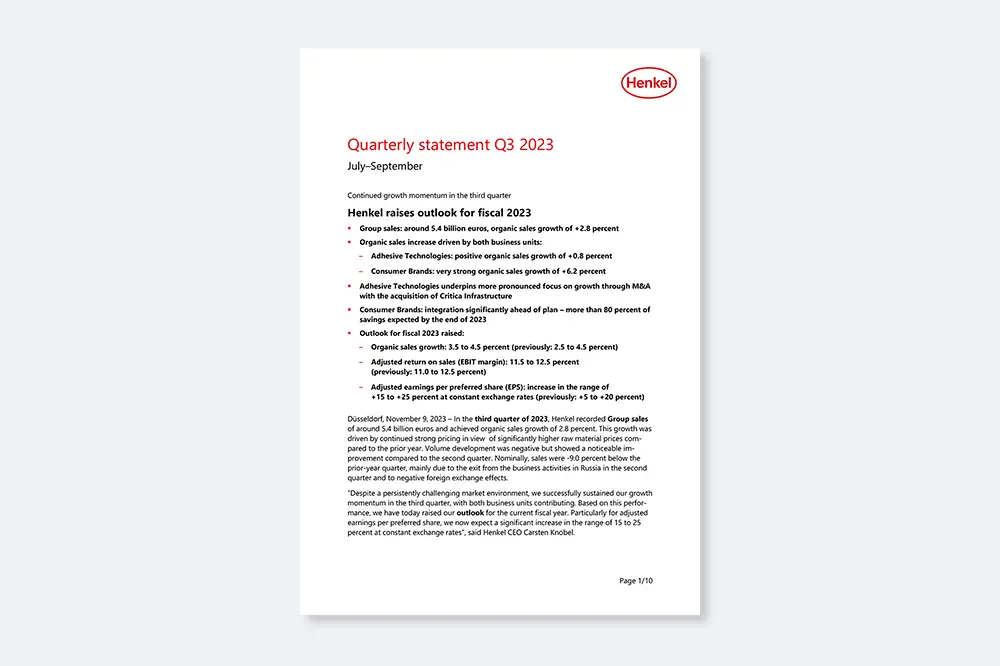

- Group sales: around 5.4 billion euros, organic sales growth of +2.8 percent

- Organic sales increase driven by both business units:

- Adhesive Technologies: positive organic sales growth of +0.8 percent

- Consumer Brands: very strong organic sales growth of +6.2 percent

- Adhesive Technologies underpins more pronounced focus on growth through M&A with the acquisition of Critica Infrastructure

- Consumer Brands: integration significantly ahead of plan – more than 80 percent of savings expected by the end of 2023

- Outlook for fiscal 2023 raised:

- Organic sales growth: 3.5 to 4.5 percent (previously: 2.5 to 4.5 percent)

- Adjusted return on sales (EBIT margin): 11.5 to 12.5 percent (previously: 11.0 to 12.5 percent)

- Adjusted earnings per preferred share (EPS): increase in the range of +15 to +25 percent at constant exchange rates (previously: +5 to +20 percent)

9 Nov 2023 Düsseldorf / Germany

Henkel raises outlook for fiscal 2023

In the third quarter of 2023, Henkel recorded Group sales of around 5.4 billion euros and achieved organic sales growth of 2.8 percent. This growth was driven by continued strong pricing in view of significantly higher raw material prices compared to the prior year. Volume development was negative but showed a noticeable improvement compared to the second quarter. Nominally, sales were -9.0 percent below the prior-year quarter, mainly due to the exit from the business activities in Russia in the second quarter and to negative foreign exchange effects.

“Despite a persistently challenging market environment, we successfully sustained our growth momentum in the third quarter, with both business units contributing. Based on this performance, we have today raised our outlook for the current fiscal year. Particularly for adjusted earnings per preferred share, we now expect a significant increase in the range of 15 to 25 percent at constant exchange rates“, said Henkel CEO Carsten Knobel.

“We have also strengthened our Adhesive Technologies portfolio with an attractive acquisition – which also reflects our more pronounced focus on growth through M&A. And we are clearly ahead of plan when it comes to the integration of our Consumer Brands business, which represents the biggest transformation of our company of the past decades.”

Sales development by business unit

Despite demand remaining subdued in some end markets relevant to Henkel, the Adhesive Technologies business unit recorded positive organic sales growth in the third quarter, driven by the Mobility & Electronics and the Craftsmen, Construction & Professional business areas. The very strong organic sales growth in the Consumer Brands business unit, which has been operating in the new set-up since the beginning of the year, was driven by the global business areas Laundry & Home Care and Hair.

“In both business units, volume development clearly improved in the third quarter compared to the previous quarter – which confirms our expectation as stated when publishing our results for the first half year. And for the quarter ahead, we expect a further sequential improvement,” Knobel added.

In addition, Henkel continued to make good progress in the third quarter with the implementation of its strategic growth agenda. By acquiring Critica Infrastructure, Henkel has added an attractive adjacent business to the portfolio of its Adhesive Technologies business unit with the aim of creating a platform for further growth: Critica is a specialized supplier for innovative composite repair and reinforcement solutions used in a wide range of industrial applications. In the Consumer Brands business unit, the integration of the consumer businesses is progressing ahead of plan. More than 80 percent of the net savings of around 250 million euros targeted in a first step by the end of 2024 are already expected to be realized by the end of 2023. Beyond that, the company has been stringently focusing its Consumer Brands portfolio on brands and products with strong margin and growth profiles.

“We have continued to consistently drive our strategic priorities in both business units in the third quarter. Thus, we remain on track to generate further growth and to expand our globally leading market positions,” said Knobel.

Group sales performance

Group sales in the third quarter of 2023 reached 5,440 million euros, a nominal decrease of -9.0 percent compared to the prior-year quarter. Effects from acquisitions and divestments – including the impact from the sale of the business in Russia – reduced sales by -5.5 percent. Foreign exchange effects also negatively impacted the sales development by -6.3 percent. Organically (i.e. adjusted for foreign exchange and acquisitions/divestments), sales increased by 2.8 percent. This growth was driven by continued strong pricing in both business units. Volumes declined year on year, yet volume development in both business units showed a noticeable sequential improvement compared to the second quarter of 2023.

Sales in the first nine months of 2023 reached 16,366 million euros, representing a nominal decrease of -3.1 percent. Organically, Henkel recorded very strong sales growth of 4.1 percent, driven by a double-digit increase in pricing.

Sales performance by region

Organic sales growth in the third quarter was driven by the Europe, North America, Latin America and IMEA regions. In contrast, organic sales development in the Asia-Pacific region was negative, mainly due to the strained market environment prevailing in China.

Also in the first nine months of 2023, the very strong organic sales growth of Henkel was driven by all regions – with the exception of the Asia-Pacific region.

Sales performance Adhesive Technologies

The Adhesive Technologies business unit generated sales of 2,711 million euros in the third quarter of 2023 (previous year: 2,995 million euros). This represents a nominal development of -9.5 percent. Organically (i.e. adjusted for foreign exchange and acquisitions/divestments), sales increased by 0.8 percent. This growth was driven by a strong increase in pricing. Volumes, by contrast, were below the prior-year level, as demand in some relevant end markets remained muted. Acquisitions/divestments reduced sales by -3.8 percent. Foreign exchange effects had a further negative impact of -6.5 percent.

In the first nine months of 2023, the Adhesive Technologies business unit reported a nominal decrease in sales of -3.3 percent to 8,186 million euros. Organically, the business unit achieved a strong increase in sales of 3.3 percent, driven by pricing.

The positive organic sales growth achieved in the third quarter was driven by the Mobility & Electronics and the Craftsmen, Construction & Professional business areas. The Mobility & Electronics business area posted very strong organic sales growth of 4.6 percent. This increase was fueled by the Automotive business, whereas performance in the Electronics business was below the prior year due to persistently muted demand. The Industrials business recorded positive organic sales growth. The Packaging & Consumer Goods business area reported an organic sales development of -5.0 percent, with sales decreasing in both the Consumer Goods and the Packaging businesses. This was due to both softer demand and high comparables achieved in the prior-year period. The Craftsmen, Construction & Professional business area generated organic sales growth of 2.8 percent, driven by the Construction and the Consumer & Craftsmen businesses. In contrast, the General Manufacturing & Maintenance business area recorded a slightly negative development as demand weakened.

From a regional perspective, performance within the Adhesive Technologies business unit in the third quarter was mixed. In Europe, organic sales development was slightly negative. Here, growth in the Mobility & Electronics and Craftsmen, Construction & Professional business areas was not able to compensate for the negative sales development registered in the Packaging & Consumer Goods business area. The North America region posted positive organic sales growth, driven by the Mobility & Electronics business area. Adhesive Technologies reached double-digit organic sales growth in the IMEA region, to which all business areas contributed. Organic sales growth was very strong in the Latin America region, driven by the Mobility & Electronics and Packaging & Consumer Goods business areas. By contrast, the Asia-Pacific region posted a decline year-on-year as all business areas were impacted particularly by the strained market environment prevailing in China.

Sales performance Consumer Brands

The Consumer Brands business unit reached sales of 2,695 million euros in the third quarter of 2023, a nominal decrease of -7.6 percent versus the prior-year quarter. Organically (i.e. adjusted for foreign exchange and acquisitions / divestments), sales increased by 6.2 percent. This growth was driven by a double-digit increase in price. By contrast, volumes decreased, also due to the ongoing portfolio optimization measures. Foreign exchange effects reduced sales by -6.3 percent and acquisitions/divestments had a negative impact of -7.5 percent.

In the first nine months of 2023, sales in the Consumer Brands business unit reached 8,060 million euros, and were thus -2.3 percent below the prior year in nominal terms. Organically, sales grew by 5.9 percent, driven by price.

The Laundry & Home Care business area generated very strong organic sales growth of 5.8 percent in the third quarter. The Laundry Care business posted a very strong organic sales increase, predominantly driven by significant double-digit sales growth in the Fabric Care category. The Home Care business delivered very strong growth too, mainly driven by a significant increase in sales in the Toilet Care category.

The Hair business area recorded significant organic sales growth of 8.9 percent in the third quarter. Within this business area, the Consumer business achieved double-digit growth, driven by the Hair Styling and Hair Care categories. The Professional business recorded very strong organic sales growth.

The Other Consumer Businesses showed a slightly negative organic sales development of -0.6 percent in the third quarter, also resulting from portfolio measures.

From a regional perspective, the Consumer Brands business unit achieved good organic sales growth in Europe in the third quarter, primarily driven by the Hair business area. The North America region recorded very strong organic sales growth, with all business areas contributing. Organic sales growth in the Latin America region was also very strong, mainly driven by the Hair business area. The IMEA region achieved double-digit organic sales growth, with both the Laundry & Home Care and Hair business areas contributing. In contrast, organic sales development in the Asia-Pacific region was below the prior-year quarter due to the Hair business area being affected by muted market development, particularly in China.

Net assets and financial position of the Group

No substantial changes to the net assets and financial position of the Group occurred in the period under review compared to the situation as at June 30, 2023.

Outlook for the Henkel Group

Based on the business performance in the first nine months of 2023 and assumptions in regard to the remainder of the year, the Management Board of Henkel AG & Co. KGaA has decided to raise the guidance for fiscal 2023.

For the Henkel Group, organic sales growth in fiscal 2023 is now expected to be in the range of 3.5 to 4.5 percent (previously: 2.5 to 4.5 percent). Organic sales growth in the Adhesive Technologies business unit is now anticipated to be in the range of 2.5 to 3.5 percent (previously: 2.0 to 4.0 percent) and in the Consumer Brands business unit in the range of 5.0 to 6.0 percent (previously: 3.0 to 5.0 percent).

For the Henkel Group, adjusted return on sales (EBIT margin) is now expected to be in the range of 11.5 to 12.5 percent (previously: 11.0 to 12.5 percent). For the Adhesive Technologies business unit, adjusted return on sales is now expected to be in the range of 14.0 to 15.0 percent (previously: 13.5 to 15.0 percent) and for the Consumer Brands business unit in the range of 10.0 to 11.0 percent (previously: 9.5 to 11.0 percent) .

The expected guidance range for adjusted earnings per preferred share (EPS) at constant exchange rates has now been raised to 15.0 to 25.0 percent (previously: 5.0 to 20.0 percent).

Furthermore, we have updated the following expectations for 2023:

- Restructuring expenses of around 300 million euros (previously: 300 to 350 million euros)

- Cash outflows for investments in property, plant and equipment and intangible assets of around 650 million euros (previously: 650 to 750 million euros)

The following expectations for 2023 remain unchanged:

- Currency impact on sales: negative impact in the mid single-digit percentage range1

- M&A impact on sales: negative impact in the mid single-digit percentage range2

- Prices for direct materials: increase in the low single-digit percentage range1

1 Compared to the prior-year average.

2 Including the effect from the exit from the business activities in Russia.

Amended reporting structure as of Q1 2023

In light of the amended reporting structure adopted as of the first quarter of 2023 (see details in Henkel’s half-year report 2023, page 5), the prior-year figures indicated for the Consumer Brands business unit, for the business areas within the two business units, and for the Europe, IMEA and Asia-Pacific regions reflect in each case the new structure.

Note: All individual figures in this document have been commercially rounded. Addition may result in deviations from the totals indicated.

This document contains statements referring to future business development, financial performance and other events or developments of future relevance for Henkel that may constitute forward-looking statements. Statements with respect to the future are characterized by the use of words such as expect, intend, plan, anticipate, believe, estimate, and similar terms. Such statements are based on current estimates and assumptions made by the corporate management of Henkel AG & Co. KGaA. These statements are not to be understood as in any way guaranteeing that those expectations will turn out to be accurate. Future performance and results actually achieved by Henkel AG & Co. KGaA and its affiliated companies depend on a number of risks and uncertainties and may therefore differ materially (both positively and negatively) from forward-looking statements. Many of these factors are outside Henkel’s control and cannot be accurately estimated in advance, such as the future economic environment and the actions of competitors and others involved in the marketplace. Henkel neither plans nor undertakes to update forward-looking statements.

This document includes supplemental financial indicators that are not clearly defined in the applicable financial reporting framework and that are or may be alternative performance measures. These supplemental financial indicators should not be viewed in isolation or as alternatives to measures of Henkel’s net assets and financial position or results of operations as presented in accordance with the applicable financial reporting framework in its Consolidated Financial Statements. Other companies that report or describe similarly titled alternative performance measures may calculate them differently.

This document has been issued for information purposes only and is not intended to constitute investment advice or an offer to sell, or a solicitation of an offer to buy, any securities.

Carsten Knobel

Marco Swoboda

1 of 2